In the past, putting down less than 20% on a house and requiring Mortgage Insurance (MI) held a negative stigma. Times have changed. In today's surging real estate market alongside escalating rents, many experts have perfected how homebuyers can use MI to their benefit. When used correctly, MI provides families with greater flexibility and buying power. Before signing another apartment lease, consider how Mortgage Insurance benefits could help you buy a house and save money.

What is Mortgage Insurance?

While putting down less than 20% on your new home may not be your ideal goal, Mortgage Insurance (MI) is available to help you bridge the gap so you can still get the home you've been dreaming of. Previously referred to as Private Mortgage Insurance — or PMI —this type of insurance is designed to protect lenders in the event a borrower defaults on their mortgage.

While lenders gain added security, borrowers who utilize MI can benefit too. Qualified borrowers can access more funds (a larger mortgage), allowing them more options when searching for their dream home. So, rather than viewing MI as a negative aspect of buying a home, it can also be a strategic tool to further your goals.

Factors That Influence the Cost of MI

The cost of MI is determined by most lenders based on the loan amount, the creditworthiness of the borrower, and the percentage of a home's value. According to the Urban Institutes Housing Finance Policy Center, the average cost of MI for a conventional home loan ranges from .466% to 1.50% of the original loan amount per year. This amount is broken down into monthly installments and added to your monthly mortgage payment.

Read the 6 Benefits of MI section below to determine if MI is worth considering based on your financial situation.

6 Benefits of MI for Home Buyers

1: Mortgage Insurance Breaks the Down Payment Barrier

Putting a 20 percent down payment was once considered the traditional way to buy a home. However, rising real estate costs and other economic factors have caused many potential home buyers to rethink this approach. Although the idea of taking on an extra home-related expense may seem counterproductive at first, a deep dive into the benefits of MI may prove otherwise.

2: MI Can Open Up More Housing Options for Qualified Borrowers*

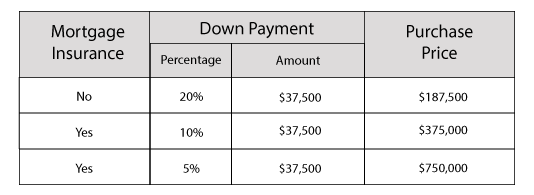

Below is an example of how MI could increase a qualified borrower’s purchasing power by more than $500,000 without changing the amount of their down payment.

Here’s the breakdown:

- 20% Down Payment and No MI: A purchase price of $187,500 less a $37,500 (20%) down payment would equate to a maximum loan amount of $150,000.

- 10% Down Payment with MI: A purchase price of $375,000 less a $37,500 (10%) down payment would equate to a maximum loan amount of $337,500. A borrower qualified for this maximum loan amount could double their buying power.

- 5% Down Payment with MI: A purchase price of $750,000 less a $37,500 (5%) down payment would equate to a maximum loan amount of $712,500. A borrower qualified for this maximum loan amount could increase their buying power by $562,500.

*NOTE: The figures in this example are for demonstration purposes and assume the borrower qualifies for the maximum loan amount stated in the breakdown above.

3: MI Is Not Permanent

For people buying a home in Massachusetts, the added expense of Mortgage Insurance could be short-lived. Lenders must automatically terminate MI when your loan balance reaches 78% of the original value of your home (or 22% equity is achieved.) However, you may not have to wait until then - if the current value of your home increases due to home improvement or market conditions - some borrowers can request (in writing) to cancel MI when a certain percentage of equity is attained, typically 20%. Details vary by lender, check with your lender to confirm.

If you're ready to become a homeowner, explore your options with our complete guide:

4: Mortgage Insurance Can Help Homebuyers Refinance an Existing Mortgage and Save

There are numerous situations in which buyers took out high-interest loans to purchase their first home. Issues such as poor credit scores, repayment blemishes, and low incomes could have been the reason. If you've diligently paid your monthly installments, refinancing with less than 20 percent equity in the house could make sense.

Make an informed financial decision, contact a Middlesex Federal Home Loan Specialist to determine if you can save money. It may even be possible to turn some of your equity into cash and use the funds to make home improvements.

5: MI Offers an Option to Renters

With the housing shortage and other factors, apartment renters are paying closer to 40 percent of their income on rent alone. According to RentHop's 2023 Singles Index, Boston ranks 4th in the nation for least affordable cities to rent. Based on the cost of a median studio rental, singles are spending an average of 37.5% of their annual income on housing.

While there are additional expenses associated with homeownership, there are also benefits. Owning a home provides you with a permanent living situation. Your landlord may increase your rent, but a fixed-rate mortgage (principal and interest) payment will remain the same for the life of the loan. Unlike a rental payment that never goes away, a mortgage payment will go away once it is paid in full. Additionally, you can build equity and use that equity to finance other expenses.

Renters should consider the overall financial benefit of becoming a homeowner and how a lower down payment and mortgage insurance could work for them.

6: Middlesex Federal Makes Mortgage Insurance Easy to Understand

While our team of experts works with Mortgage Insurance daily, we understand the nuances of MI can be confusing. We take the time to simplify MI and every other step of the home-buying process. Whether this is your first, second, or investment home, we are ready to help you achieve your goals.

Contact a Middlesex Federal Home Loan Specialist to discuss MI and evaluate your home buying options.

Questions about Mortgage Insurance? We Can Help!

Everyone deserves an opportunity to realize the dream of homeownership, and for qualified borrowers, Mortgage Insurance can be a valuable tool. If you are ready to stop paying rent or want to see if homeownership is possible, we're prepared to help! Get in touch with a Middlesex Federal Home Loan Specialist today!

![How to Increase the Value of Your Home [Expert Advice Checklist]](https://blog.middlesexfederal.com/hubfs/two-businesspeople-working-laptop.jpg)

SHARE